In this article

Fraud analytics software has become a board-level priority, yet the teams expected to deliver fraud detection capability are often the furthest from having it. If you lead an internal audit function at a large or enterprise organization, you know the gap firsthand. Your audit committee wants continuous fraud monitoring. Your board expects data-driven insights. And your team is still pulling transaction extracts into Excel and testing only part of ERP data each quarter.

The risk backdrop is not theoretical. The ACFE's 2024 findings put the median loss per occupational fraud case at $145,000. Boards are asking for continuous, AI-accelerated oversight while audit teams are still operating with tools and methods designed for periodic, sample-based testing.

This guide is for teams that need to move from sampling to full-population testing, from periodic checks to continuous monitoring and from manual analysis to AI-accelerated fraud analytics. It is built for chief audit executives, heads of risk, CFOs and the senior auditors who do the hands-on work — not financial crime operations teams running AML transaction monitoring.

This guide covers:

Fraud analytics software is a category of purpose-built platforms that apply data analysis, pattern recognition and increasingly AI to detect fraud, anomalies and control failures across financial transactions. These platforms enable audit, risk and finance teams to test entire data populations rather than relying on sampling.

The critical distinction matters more than most buyer's guides acknowledge. Generic BI and data visualization tools can visualize data, but they lack built-in fraud detection scenarios, audit-grade evidence trails, continuous monitoring automation and GRC-specific workflows. The IIA's Global Model Internal Audit Curriculum treats this difference explicitly, positioning purpose-built audit analytics tools specifically for fraud detection and control testing while categorizing BI tools as a visualization layer.

Transaction monitoring platforms built for AML and KYC focus on real-time payment screening and are architected for banking compliance, not internal audit. They produce regulatory outputs like suspicious activity reports, not audit workpapers. So if your goal is testing controls and producing audit-ready evidence, AML and KYC platforms aren't the category to shortlist — they're sold to compliance operations teams in banks, not to internal audit.

Fraud analytics software for GRC sits between these categories: deep analytics on complete structured data, built-in fraud scenarios, continuous automation and audit-ready output. It is designed from the ground up for scripted and repeatable tests, exception tracking, SOX and ICFR alignment and results that can be reported directly to audit committees and boards.

Choosing the right platform requires evaluating capabilities against the specific needs of audit, risk and finance teams. Feature lists are necessary but insufficient. The evaluation framework below is grounded in professional standards from the IIA and ISACA, and structured around the criteria that matter most to CAEs, CROs and CFOs.

Start with your organization's actual fraud risk landscape. Map your highest-risk processes: accounts payable and vendor fraud, T&E anomalies, payroll irregularities, access control violations. Match tool capabilities to actual risk exposure, not a generic feature matrix.

The shift from sample-based testing to analyzing every record is the single biggest capability gap most audit teams face. ISACA's updated ITAF update reflects the profession's shift toward data-driven audit approaches.

Evaluate whether the platform supports full-population data ingestion, scripted and repeatable tests and the ability to move from periodic sampling to continuous oversight. This is no longer merely aspirational; it is increasingly expected in modern audit practice.

Fraud analytics platforms use machine learning for anomaly detection, pattern recognition and predictive scoring. Evaluate whether the platform offers no-code natural language interfaces that don't require data science skills, whether AI outputs are transparent and explainable with full logs and whether the AI operates within controlled and auditable guardrails that audit committees can trust.

ISACA's guidance on AI audit guidance is direct: auditors must "use AI ethically, transparently and within the bounds of professional standards and regulatory frameworks." According to What Directors Think 2026 by Diligent Institute and Corporate Board Member, only 22% of directors say their boards have AI governance processes for board AI usage. That makes AI governance maturity a practical evaluation criterion, not just a future consideration.

For CAEs and compliance leads, the platform must produce audit-ready evidence, not dashboards. Evaluate audit trails, exception tracking, version-controlled test scripts and alignment with SOX, ICFR, COSO and NIST frameworks. Can the platform document testing methodology for external auditors and regulators? Can evidence packages be exported in formats acceptable under PCAOB standards?

Explore opportunities for automation related to the management of the SOX framework by using a GRC technology platform. In practice, that means looking for workflow support for control testing, deficiency remediation, ongoing monitoring and clear accountability.

Evaluate connectors to ERP systems (SAP, Oracle, NetSuite, Microsoft Dynamics), HR and payroll platforms and AP and T&E systems. Continuous monitoring requires automated data ingestion, not manual exports. Assess whether the platform supports scheduled robots that pull data, run tests and flag exceptions without analyst intervention.

According to the Transaction Readiness Report by Diligent Institute and partners, only 4% of organizations have fully integrated GRC and financial systems. That gap is a practical reason to evaluate integration and automated data access early rather than treating them as secondary requirements.

Frame evaluation around provable ROI, not license cost alone. Ask for deployment timelines and documented customer results that show the path from implementation to first findings. A common proof-of-value path is AP duplicate payment testing because it can surface exceptions and demonstrate the value of moving beyond manual review.

Building trust in data and risk reporting can help organizations have more productive conversations and drive change.

Learn how leading companies identify and address risks before they become problems.

Most lists ranking the best fraud detection software or top fraud detection software focus on features in isolation. For GRC teams, the strongest platform is one that fits into audit, risk and finance workflows and produces results that withstand audit committee and regulatory scrutiny.

The strongest fraud analytics platform for GRC delivers:

The value of fraud analytics software is measured in the specific risks it helps teams detect, investigate and prevent. These use cases represent the fraud scenarios that audit, risk and finance teams encounter most frequently across enterprise organizations.

AP fraud is the highest-volume, highest-impact fraud risk for most organizations. Fraud analytics software flags duplicate payments across large transaction volumes, identifies vendor master anomalies (shared bank accounts, PO box addresses, dormant vendors reactivated before large payments) and surfaces overpayments that manual review would miss.

Specific tests include matching employee addresses and bank accounts against vendor records, applying Benford's Law to invoice amount distributions and tracking payment escalation patterns.

A focused AP analytics program can also produce clear business value early. For audit and finance leaders, that is a strong example of why duplicate payment testing is often the right first fraud analytics use case: the risk is easy to understand, the data is usually available and the results can be measured quickly.

T&E anomalies include duplicate expense claims, round-number submissions, weekend and holiday charges, high-risk merchant categories and split transactions designed to stay under approval thresholds.

Ghost employees can persist undetected for extended periods. Tests include identifying duplicate bank account numbers across payroll records, flagging payments to individuals not in the HR master file and detecting employees with no benefits enrollment.

Segregation of duties violations, leavers with active system access, privileged access outside role requirements and access changes that coincide with suspicious transactions. The IIA's GTAG 13 states that "to test and monitor internal controls effectively, organizations should analyze all relevant transactions against control parameters, across all systems and all applications."

The shift from periodic fraud testing to continuous, automated monitoring is where the greatest risk reduction occurs. Use that finding to support a focused pilot in one high-risk process such as AP, T&E, payroll or access data, then compare exception volume and manual review effort before and after automation to show the value of moving beyond periodic sampling.

Audit and risk teams are interested in AI for fraud detection but concerned about transparency, hallucinations, skill gaps and implementation complexity. These concerns are well-founded. Generic AI assistants were not built for audit work.

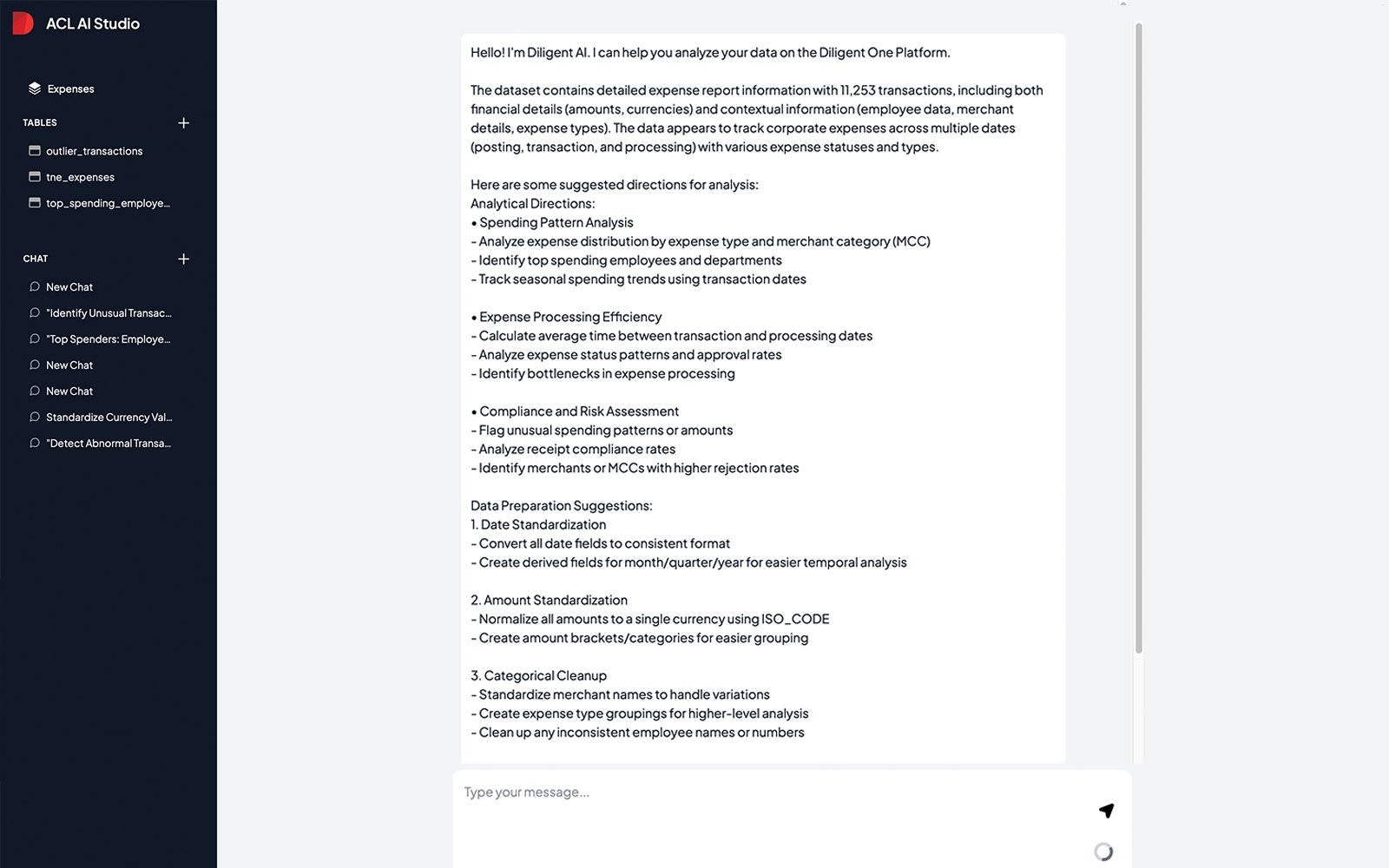

ACL Analytics is Diligent's analytics platform for audit, risk and compliance teams. It analyzes complete transactional data from any structured source (ERP, AP, HR, T&E), runs pre-built fraud scenarios and supports both no-code interfaces for audit generalists and full scripting capabilities for advanced users.

ACL AI Studio layers on top of existing ACL Analytics workflows, adding natural language queries that translate into auditable test logic, transparent logs that show exactly how results were derived and no black-box model outputs.

Unlike generic AI tools that may hallucinate results, AI Studio is presented as operating within an integrated platform designed to ensure data security and privacy. The Diligent One Platform connects analytics and findings to risk registers, audit workflows and board-ready reporting.

This capability aligns with board-level demand and can help teams position AI-powered fraud analytics as a governance and assurance capability, not just a technical upgrade. Use that board interest to support executive sponsorship for analytics investments and to frame AI adoption around transparency, auditability and faster oversight.

Three common objections addressed directly:

"We don't have the coding skills." AI Studio's natural language interface means auditors describe what they want to test in plain English, and the platform generates the analytics logic.

"We can't trust AI for audit work." Diligent's AI tools provide strong audit-trail and documentation features, such as logging every prompt and maintaining audit-ready records of analytics activity, but product documents do not state that every AI-generated analysis always produces a full audit trail detailing the query, the logic applied, the data sources accessed and the results.

"Implementation will take months." ACL Analytics desktop can be deployed without replacing existing workflows. AI Studio layers on top of existing ACL workflows, not beside them.

See how an enterprise telecom modernized internal audit with ACL Analytics and cut audit timelines by a third.

The best proof of value comes from teams that have already made the shift from manual, sample-based fraud testing to automated, continuous analytics.

Siemens Financial Services Inc. implemented ACL Analytics to shift from manual control processes to continuous assurance across its operations. By digitizing control processes, the company achieved a 90% reduction in the time needed for ICFR testing, allowing the team to reallocate resources to more strategic initiatives.

The platform's ability to analyze 100% of transactional data moved the team beyond the limitations of traditional sampling techniques, providing more rigorous and accurate assessment of control effectiveness while significantly mitigating the risk of undetected errors or inconsistencies.

Teachers Mutual Bank Limited, one of the largest customer-owned banks in Australia, used Diligent's Internal Audit Management and ACL Analytics solutions to deliver a centralized and streamlined audit process. The implementation achieved a significant reduction in manual tasks for auditors and auditees while improving stakeholder relationships through enhanced collaboration and business transparency. The team gained superior, one-click reporting for the audit committee and business.

An enterprise telecommunications company modernized its audit team's operations by moving off spreadsheets and into an integrated solution with Diligent's Internal Audit Management and ACL Analytics. The company cut audit timelines by a third, demonstrating the efficiency gains possible when teams shift from manual processes to purpose-built fraud analytics platforms.

These implementations share common patterns: organizations moved from periodic, sample-based testing to continuous monitoring; teams reallocated time from manual data preparation to higher-value analysis; and audit committees received more frequent, data-driven insights.

Moving from manual processes to fraud analytics doesn't require a multi-year transformation. The most successful implementations start with a focused pilot that proves value fast, then expand.

Foundational analytics: Teams still in Excel, manual scripts or basic BI, running sample-based fraud checks. The first step is moving to a purpose-built platform that can ingest full data populations and run repeatable tests. Start here if your team has never tested the full transaction population.

Structured fraud analytics: Move into purpose-built fraud analytics with scripted tests (duplicate payments, T&E anomalies, access violations) and scheduled continuous monitoring. Tests run automatically, exceptions are tracked and results feed audit committee reporting. This is an aspirational target for where enterprise audit teams should be operating.

AI-accelerated analytics: Layer on AI-accelerated analytics and integrated GRC platforms to enable natural-language fraud analytics, cross-system monitoring and automated workflows that connect fraud findings to risk registers and board materials.

Pick one high-impact use case: Duplicate AP payments are a common starting point because they involve high transaction volume, clear financial impact and can offer fast proof of value. Multi-ERP environments are especially strong candidates because manual processes cannot catch cross-system duplicates.

Identify minimum data and stakeholders: Which systems (ERP, AP, T&E), who needs to be involved (audit lead, finance contact, IT or data owner for system access). Define your baseline: current manual testing hours, sample sizes and coverage percentages.

Run the pilot: Ingest historical AP data. Run duplicate payment detection, Benford's Law analysis and vendor master anomaly tests across the full population. Document current vs. improved coverage: from testing 200 out of 200,000 transactions to analyzing all 200,000.

Report results: Present findings to the audit committee with quantified outcomes: hours saved, dollar value of exceptions identified and percentage of data now covered versus prior sampling approach. Use the proven results above to benchmark expectations and demonstrate ROI.

For teams at the foundational stage, start a free 30-day trial of ACL Analytics focused on one or two fraud use cases.

For teams ready for continuous monitoring and AI capabilities, book a fraud analytics discovery session to map out ACL Robotics and ACL AI Studio opportunities across AP, payroll, T&E and access controls.

Internal audit teams use fraud detection software to run tests across AP, T&E, payroll and access control data. Common applications include identifying duplicate payments, flagging suspicious vendor activity, detecting phantom employees and monitoring segregation of duties violations. A key driver of adoption is the move from sample-based testing to full-population analytics.

For GRC use cases, yes. Purpose-built fraud analytics platforms include pre-built fraud scenarios, scripted test libraries, continuous monitoring robots and audit-grade reporting that generic BI tools don't offer. Generic BI tools require analysts to build fraud logic from scratch and produce visualizations rather than audit evidence.

GRC-specific AI fraud analytics platforms are designed to provide explainable outputs and strong audit-trail capabilities, such as logging prompts, generated logic and results. GRC-grade platforms are intended to support audit committee review and regulatory compliance, but buyers should verify the exact level of traceability during evaluation.

The best fraud detection software for audit and risk teams offers full-population data analysis, pre-built fraud scenarios, continuous monitoring automation, transparent AI capabilities and audit-grade evidence production. The platform should integrate with existing ERP, AP and HR systems and produce results reportable directly to audit committees and boards.

Fraud analytics software for GRC is designed for internal audit, risk and finance teams to test transactional data, detect anomalies and produce audit-ready evidence. Transaction monitoring platforms built for AML and KYC focus on real-time payment screening for banking compliance. The buyers, use cases and outputs differ: fraud analytics platforms produce audit workpapers and exception reports for audit committees, while AML and KYC monitoring platforms produce suspicious activity reports for regulators.

ACL Analytics desktop can be deployed in hours to days for immediate testing of AP duplicate payments, T&E anomalies or access violations. AI Studio adds natural language capabilities on top of existing ACL workflows within days. Early fraud and overpayment wins typically surface within the first 30-60 days, as demonstrated by customer implementations like Siemens Financial Services (90% faster ICFR testing) and the enterprise telecommunications company (one-third faster audit timelines).

Ready to move from sampling to continuous monitoring for fraud analytics? Start an ACL Analytics trial or book a discovery session with an ACL specialist.